Making Tax Digital (MTD) represents a fundamental shift in how HMRC expects individuals and businesses to manage tax records. While many believe digital tax filing is unavoidable, HMRC provides specific exemptions for those unable to comply. At CMA Accountancy, we provide tailored guidance to ensure taxpayers understand their eligibility and the options available under current regulations.

Understanding Who Qualifies for MTD Exemptions

Exemptions are available under HMRC rules for individuals facing genuine barriers to digital compliance. These include health-related limitations, accessibility issues, and specific personal circumstances.

Health, Disability, or Age-Related Exemptions

Individuals who cannot use digital tools due to physical or mental health conditions may qualify. This includes:

- Severe visual impairment or blindness

- Arthritis or conditions affecting hand dexterity

- Cognitive impairments or mental health conditions

- Long-term hospitalisation or incapacitation

These exemptions require evidence, such as medical documentation, demonstrating the inability to engage with MTD-compliant software or online submissions.

Revenue breakdown

Remote Location and Internet Accessibility Issues

MTD requires reliable digital access. Taxpayers in areas lacking consistent internet connectivity may be eligible for exemption. HMRC requires that individuals demonstrate:

- No access to internet services at home

- Inability to reach a public internet facility within reasonable distance

Such exemptions are particularly relevant for rural residents with limited infrastructure.

Religious or Cultural Restrictions

Where religious beliefs prevent the use of electronic devices or online communication, HMRC may grant exemptions. This is applicable when the faith of the taxpayer strictly prohibits engagement with digital technology.

Severe Circumstances and Mental Capacity

Exemptions also cover extreme situations, including:

- Individuals lacking mental capacity to manage tax affairs

- Those who are functionally illiterate or unable to engage with financial records

- Residents of long-term care facilities unable to interact with digital systems

Automatic Exclusions

Some taxpayers are automatically excluded from MTD, including:

- Trustees or personal representatives managing deceased estates

- Non-resident companies

- Certain members of Lloyd’s underwriting businesses

- Individuals without a National Insurance number by January prior to the tax year

These automatic exclusions simplify compliance requirements for complex or specialised circumstances.

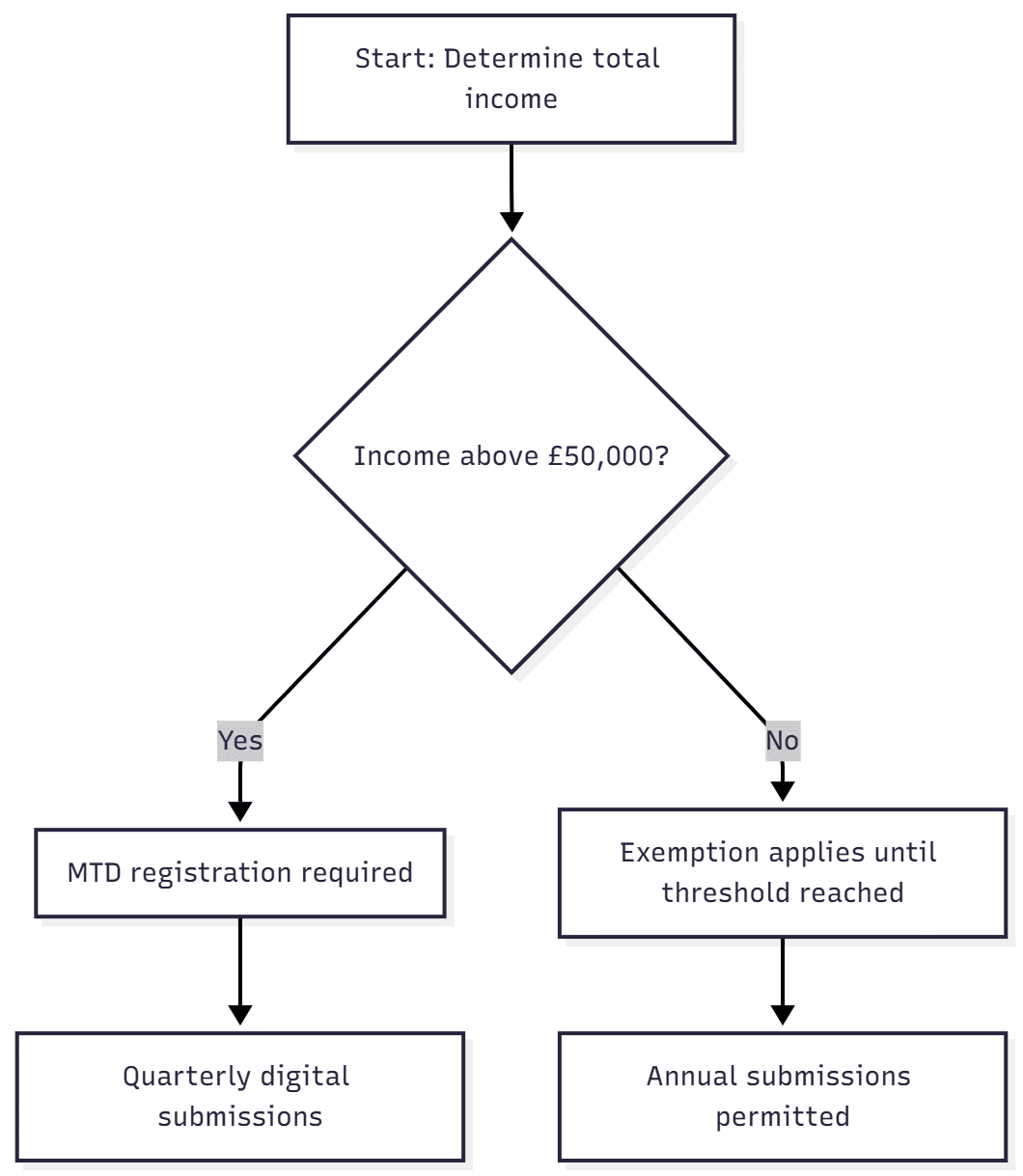

Income Thresholds and the Gradual Rollout of Making Tax Digital

MTD for Income Tax is initially applied to taxpayers with income above specific thresholds. For example:

- 2024–25: £50,000 gross income from self-employment and property

- 2025–26: £30,000 threshold

- 2026–27 onwards: £20,000 threshold

Taxpayers below these thresholds are not required to participate, providing a phased approach for small businesses and self-employed individuals.

Practical Guidance for the Self-Employed

Self-employed individuals often face complex decisions regarding MTD compliance. At CMA Accountancy, we advise maintaining clear separation between business and personal expenses, using suspense accounts for transactions requiring review before final categorisation. This ensures accurate reporting and mitigates risk of errors during digital submissions.

Structuring for Compliance Flexibility

Currently, MTD rules do not apply to partnerships. Forming a partnership with a spouse or associate can allow continued annual filing instead of quarterly submissions. While HMRC may extend MTD to partnerships in the future, this remains a legitimate temporary measure for managing administrative burden.

MTD is a permanent fixture in the UK tax landscape, yet exemptions exist for those with legitimate reasons. Health conditions, remote living, religious beliefs, and income thresholds are key considerations. CMA Accountancy provides expert guidance, helping taxpayers assess eligibility, optimise business structures, and ensure compliance without unnecessary disruption.

For professional advice on MTD exemptions or business structuring, CMA Accountancy offers bespoke support to navigate HMRC rules confidently.